Who Reports Your Crypto to the Spanish Tax Agency (and What They Send): A Business Expats Guide for Exchange Users

- Business Expats

- Sep 26, 2025

- 3 min read

If you trade crypto on an exchange or hold assets with a custodian, part of your activity may be reported to the Spanish Tax Agency (AEAT) through two informational filings: Model 172 (balances) and Model 173 (transactions). The key issue is not how much you trade, but who provides the service and from where.

Who is obliged to report in Spain?

The obligation applies to individuals or entities resident in Spain and to permanent establishments (PEs) in Spain of foreign entities that provide services of:

Custody (safekeeping of private keys), or

Exchange/intermediation between crypto↔fiat or crypto↔crypto.

Model 172 covers balances, and Model 173 covers transactions. Both are annual and filed in January with data from the previous year.

What is reported under Model 172 (balances as of 31/12)?

For each user and for each token:

Identifying data (name, NIF/NIE, address),

Units held, and

Valuation in euros at 23:59 on December 31.

If the custodian also holds fiat on your behalf, the balance and the exchange rate applied are reported. The reporting entity must also specify the pricing source used (platform or price tracker).

What is reported under Model 173 (all transactions)?

Every purchase, sale, swap, and transfer must be reported, including:

Type and date of the transaction,

Token and units,

Value in euros,

Commissions, and

Where applicable, the nature of the consideration (fiat, another crypto/asset, goods/services, or a combination).

New development: Transfers between internal wallets and with external wallets must also be reported (outflows with negative value; inflows with positive value).

What if my exchange is foreign?

If your provider is not resident in Spain and has no permanent establishment in Spain, it does not file Models 172/173 for that activity. In such cases, the obligation to declare foreign-held crypto may fall on you personally, through Model 721.

How to know if “your” exchange reports?

Check whether it has a Spanish company, branch, or PE (Spanish NIF, local address in T&Cs, invoices with NIF ES).

Verify whether it appears in the MiCA registry of the CNMV as a CASP (crypto-asset service provider) authorized to operate in Spain. They may operate via “passporting” from another EU country, but the 172/173 obligation depends on whether they provide custody/exchange services from Spain (residence or PE).

Relevant examples today

Bit2Me (Spain): Authorized by CNMV under MiCA to operate as a CASP. If it provides custody/exchange services from Spain, it falls under 172/173 reporting.

The CNMV list also includes BBVA, Openbank, Coinbase Luxembourg S.A., Bitstamp Europe S.A., Bitvavo B.V., Bybit EU GmbH, BitGo Europe GmbH, among others, which may provide services in Spain (often through passporting from another Member State). If they lack a Spanish PE, they are not automatically obliged to file 172/173 in Spain.

What does this mean for you?

If you use a provider with a tax footprint in Spain that offers custody or intermediation, the Tax Agency will receive your balances (172) and transactions (173) in standardized XML format — your Spanish income tax return (IRPF) must align with this traceability.

If you operate only with platforms that have no residence/PE in Spain, review your potential Model 721 obligation and maintain evidence (statements, hashes, pricing sources) to ensure proper alignment of your tax reporting.

Business Expats solution

At Business Expats, we verify your specific exchange (residence/PE, MiCA status, reporting obligations) and provide you with a 172/173 reconciliation template for your IRPF — ready to use.

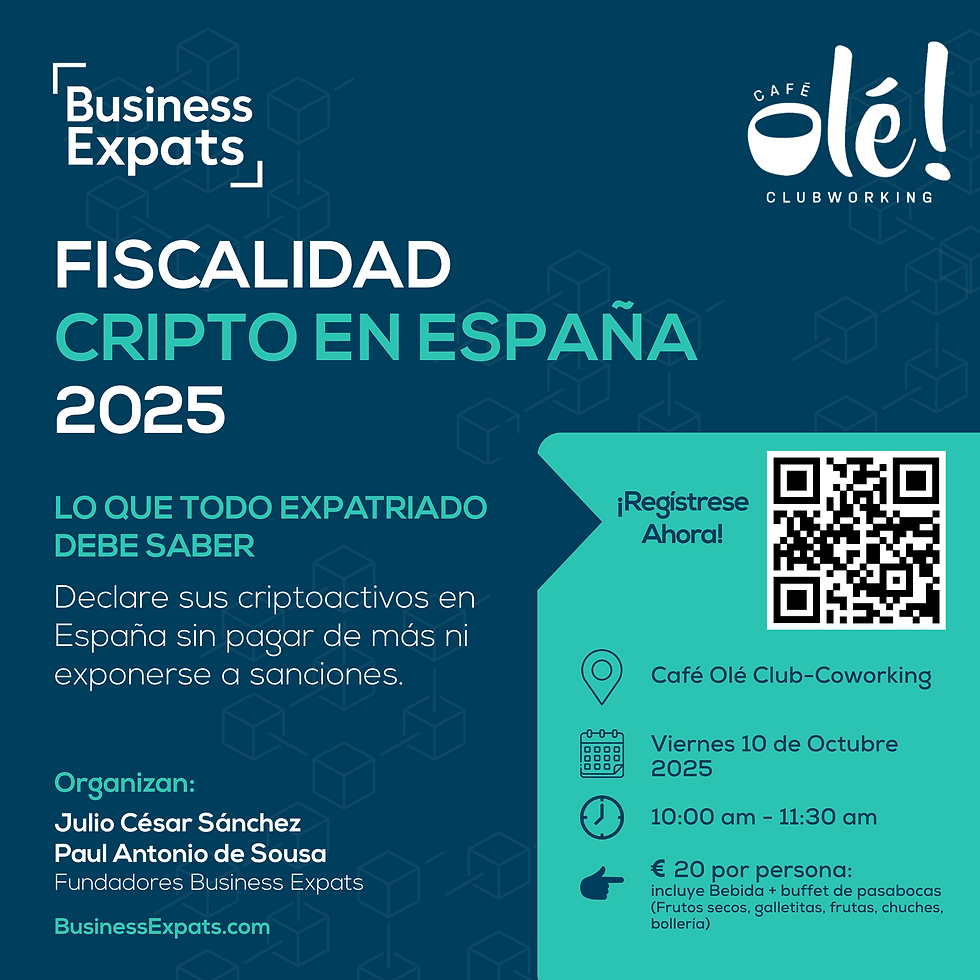

Final Reminder

On October 10, join us at Café Olé (Madrid) for a practical session on MiCA, Models 172/173, and Model 721: what the Spanish Tax Agency sees, how valuations are determined, and how to safeguard your traceability effectively.

Will wait to see you there,

Comments